Information Hub

Choosing a Nursing Home

“It looked like a four star hotel, with flowers in the foyer and art on the walls but the problems began straight away for my mother”

Bill Lawrence

There are so many considerations when selecting a nursing home as Bill Lawrence found out to his detriment, so much so he decided to write a book about it. He describes his experience as “the most stressful time of his life”. Back then his mother moved into a nursing home and he was trying to source the perfect nursing home for his mother but found the opposite.

Fair Deal Information

The Fair Deal Scheme (also known as the Nursing Home Support Scheme) was introduced in 2009 to provide financial support for people that require long term care in a nursing home. The general rule is simple: the more assets and income you have, the more you will pay toward your care. The process consists of two main stages once you’ve completed the application form:

- Care Needs Assessment

This stage examines whether long term care in a nursing home is required.

- Financial Assessment

At this stage, your income and assets will be reviewed to determine if you are eligible for financial support, and if so, how much support you will require.

- Care Needs Assessment

This assessment is carried out by a qualified medical professional who will determine whether you require long term care in a nursing home. This assessment may take place either in your home or in a hospital, depending on your situation.

- Financial Assessment

The HSE will assess you regular income and assets to determine whether you qualify for the scheme and if so, what your contribution will be.

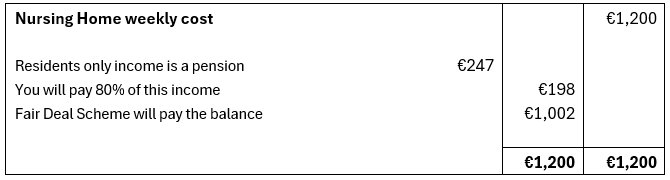

Income

80% of all your regular income will go towards your long-term care.

Regular income can include sources such as pension payments, rental income, social welfare payments, and other recurring earnings.

What does this mean?

If I am single person and I have a regular weekly income of €1,000 I will be required to contribute €800 towards my nursing home care weekly.

It’s important to note that rental income from your main home may be exempt from consideration, but only if it meets specific criteria set by the Fair Deal Scheme.

Assets

7.5% of your assets will go towards you long term care.

Your assets could include your home, cash savings, development property, farms, business etc. The first €36,000 of your assets is exempt. This amount will be deducted first from your cash assets, with any remaining balance being deducted from your other assets.

Furthermore, there is a 3-year cap on your home i.e. the maximum contribution you will make on your home is 22.5% of the value, this applies from the date you enter the nursing home. This means if your home is valued at €350,000 you will only pay a maximum of €78,750 (22.5% of 350,000)

If Assets are sold or transferred 5 years prior to the application date they are included in the assessment.

If you have a partner your contribution will be 3.75% and your exemption will be €72,000.

Optional – Nursing Home Loan

Another option is to defer your contribution related to your home through the Nursing Home Loan (also known as the Ancillary Loan). For example, if the total repayment due to the HSE is €78,750 (350,000 * 22.5%), this amount can be deferred until after your loved one’s passing. However, you will be required to repay the loan within 12 months after the resident is deceased. This may require selling the house to cover the loan.

Interest will be charged after 12 months, and the loan is also subject to changes based on the Consumer Price Index (CPI), which can reflect inflation or deflation.

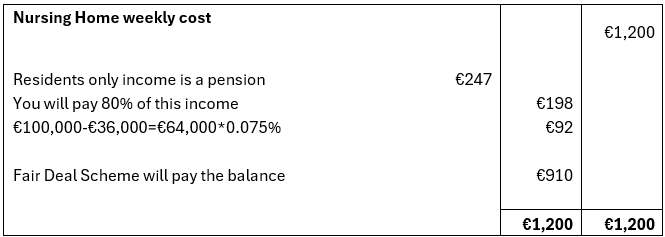

Part B) Pension Income Only & Cash Asset

This becomes more complicated if the resident has more income or owns assets.

In relation to cash in the bank the threshold is €36,000 per person. That is to say that you could have €36,000 in the bank and still qualify for the fair deal scheme mentioned above (€72,000 per couple).

Taking this further, everything over €36,000 carries a notional income of 0.075%.

Let’s say you have €100,000 in the bank. Adapting the above format would mean that:

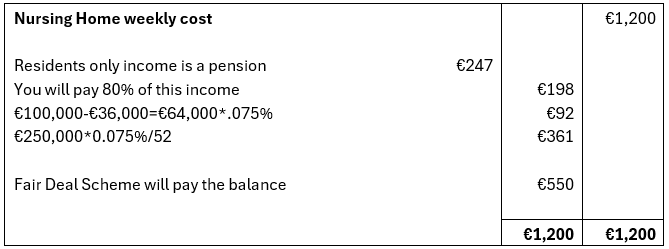

Scenario 2

Now we look at an example where you also own a house.

Let say that this Principal Private Residence (PPR) is worth €250,000 and you are the sole occupant.

The rule is that all assets are calculated at 0.075% of their value and are classed as notional income.

See example below;

Your PPR stays on the fair deal equation for 3 years.

This means that after 3 years the value of your house and its notional income fall out of the calculations and the Fair Deal contribution will go up.

In addition, there are other complications where your spouse is still living in the PPR, or indeed if you have family living in the house. Adjustments are made for these eventualities.

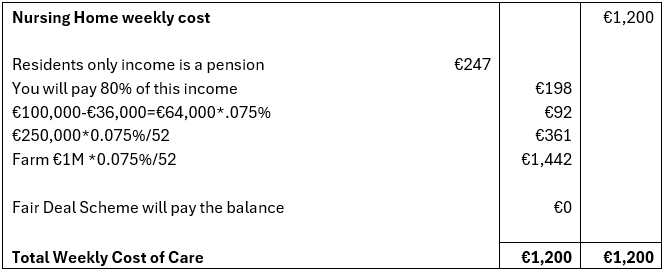

Scenario 3

To take another example, the resident has a farm of land (100 acres @ €10,000 per acre = €1M) and a private pension €200 per week (€100,000 in the bank and PPR worth €250,000 as above).

In this case your income and assets are too high so the Fair Deal Scheme would pay nothing. However, if farmers meet certain criteria, the value of the farm may be excluded from the calculations.

Example Four – Auxiliary Loan Scheme

However, let’s take another example where the same farmer has no money in the bank and only lives off the state pension i.e. asset rich and cash poor.

For scenarios like this, there is an additional scheme added to the fair deal scheme titled Auxiliary Loan Scheme. This is a facility whereby the resident pledges 22.5% of the value of their assets to the exchequer on the basis that the Fair Deal Scheme will cover their cost of care. Effectively this a loan from the state using your assets as security and it’s repaid from your estate. This would entail engaging with your solicitor to register a charge on your assets.

This is an excellent facility for those who do not want to undergo the stress of having to sell the homestead/family business just to raise funds to pay for cost of care.

This is designed to protect farms and businesses and keep them viable for the next generation.